Honasa Consumer Q4 Profit Surges to Rs 69.43 Crore; Declares Maiden Final Dividend

India’s digital-first beauty and personal care sector is entering a more mature phase, and Honasa Consumer appears determined to signal that transition with profitability, scale, and shareholder returns.

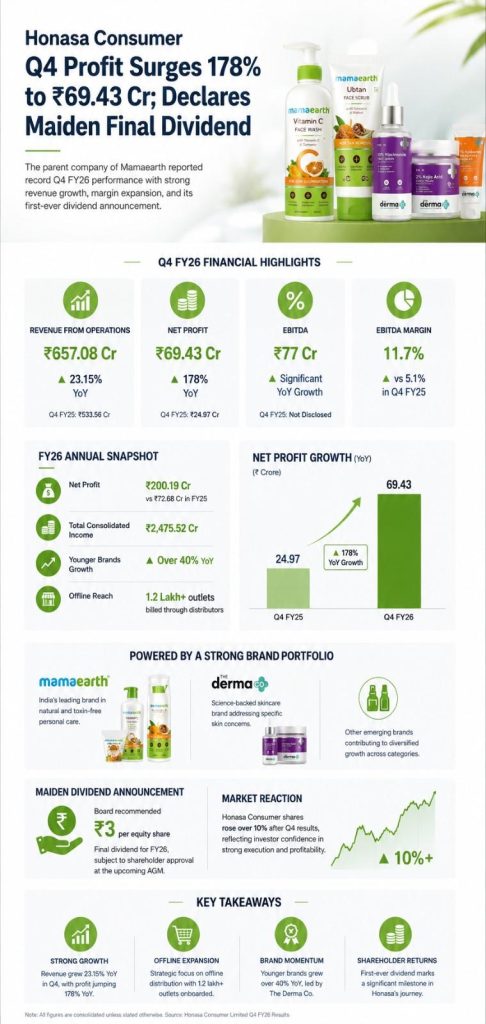

The parent company of brands including Mamaearth and The Derma Co reported a sharp rise in fourth-quarter earnings for FY26, posting consolidated net profit of Rs 69.43 crore, up nearly 178% year-on-year from Rs 24.97 crore in the corresponding quarter last year. The company also announced its maiden final dividend of Rs 3 per equity share.

The earnings reflect a broader operational turnaround for the company after a volatile period following its public listing. Improved margins, stronger offline execution, and sustained momentum in newer brands helped the company deliver its highest-ever quarterly revenue and EBITDA performance.

Record Quarterly Performance Marks a Strategic Shift

Honasa Consumer’s revenue from operations rose 23.15% year-on-year to Rs 657.08 crore during the March quarter, compared with Rs 533.56 crore a year earlier. EBITDA climbed sharply to Rs 77 crore, while EBITDA margins expanded to 11.7% from 5.1% in the previous year period.

The numbers are significant not merely because of the growth rate, but because they indicate improving operating discipline in a category where customer acquisition costs, influencer-led marketing, and discounting pressures have historically weighed heavily on profitability.

According to the company, FY26 marked the third consecutive quarter of revenue growth exceeding 20%, suggesting the recovery is becoming more structural rather than seasonal.

For the full financial year FY26, Honasa Consumer reported:

- Net profit of Rs 200.19 crore, compared with Rs 72.68 crore in FY25

- Total consolidated income of Rs 2,475.52 crore

- Significant expansion in operating margins and cash generation

The board recommended a final dividend of Rs 3 per share, amounting to roughly 51.2% of FY26 standalone profit after tax. The payout remains subject to shareholder approval at the company’s annual general meeting.

Offline Distribution Is Becoming a Core Growth Engine

One of the most important takeaways from Honasa’s latest results is the increasing role of offline retail.

The company stated that it directly billed around 1.2 lakh outlets through distributors during FY26 as part of its broader distribution expansion strategy.

That shift matters because India’s beauty and personal care market remains heavily dependent on physical retail, particularly outside metro cities. While Mamaearth initially gained traction as a digital-native brand leveraging influencer marketing and e-commerce channels, long-term scale in FMCG still depends on retail penetration, shelf visibility, and general trade execution.

Industry analysts have repeatedly pointed out that sustainable FMCG success in India typically requires a balanced omnichannel strategy rather than excessive reliance on online marketplaces.

Honasa appears to be moving in that direction.

The company’s focus on rebuilding offline momentum comes after earlier investor concerns around slowing growth and profitability pressures post-listing. Over the past year, management has emphasized sharper category execution, hero-product scaling, and distribution efficiency improvements.

The Derma Co and Younger Brands Continue to Scale

Another key driver behind the company’s improved performance has been the rapid growth of its newer brands.

Honasa said its “younger brands” grew over 40% year-on-year during FY26.

Among them, The Derma Co continues to emerge as a standout performer. The active skincare segment in India has expanded rapidly over the last three years, fueled by rising consumer awareness around ingredients, dermatology-backed products, and science-led skincare routines.

Unlike traditional mass-market beauty positioning, brands such as The Derma Co target younger consumers looking for ingredient-specific solutions including niacinamide, salicylic acid, and retinol-based products.

This mirrors a broader global shift in skincare consumption where efficacy-focused products are gaining share from purely cosmetic positioning.

For Honasa, this diversification reduces overdependence on Mamaearth while strengthening its presence across multiple beauty and personal care subcategories.

Market Response Signals Renewed Investor Confidence

Investor sentiment turned sharply positive following the earnings announcement.

Honasa Consumer shares rose more than 10% in early trade after the results, with several brokerages maintaining bullish views on the company’s long-term growth trajectory.

Brokerage firms including Jefferies reportedly retained positive ratings, citing stronger execution, improving profitability, and expanding distribution capabilities.

The maiden dividend announcement also carries symbolic importance.

High-growth consumer internet and D2C companies are often evaluated primarily on revenue expansion rather than capital returns. By initiating a dividend, Honasa is signaling growing confidence in cash flows, balance sheet strength, and earnings sustainability.

That could help reposition the company in the eyes of institutional investors who increasingly prioritize profitability alongside growth.

India’s Beauty and Personal Care Market Is Entering a Consolidation Phase

Honasa’s results also reflect larger shifts taking place within India’s beauty and personal care ecosystem.

Over the past decade, the sector witnessed a wave of digitally native brands fueled by venture capital, influencer-led marketing, and rapid online customer acquisition. However, rising advertising costs, increased competition, and profitability concerns have made scale harder to achieve.

The market is now moving toward a more disciplined phase where operational efficiency, repeat purchase behavior, offline distribution, and margin expansion are becoming critical differentiators.

Legacy FMCG players such as Hindustan Unilever, Dabur India, and Godrej Consumer Products continue to intensify competition in premium skincare and personal care categories, while newer startups face funding normalization pressures.

In that environment, Honasa’s ability to improve profitability while maintaining double-digit growth could strengthen its positioning within the sector.

Challenges Still Remain

Despite the strong quarter, challenges remain for Honasa Consumer.

The beauty and personal care industry remains highly competitive, particularly in skincare and premium wellness categories. Customer loyalty can shift quickly, and sustaining growth often requires continuous investment in innovation, branding, and retail expansion.

Margin sustainability will also be closely watched. Input cost volatility, rising competitive intensity, and marketing spend requirements could affect future profitability.

Additionally, as the company scales offline distribution, execution complexity increases significantly. Managing channel partnerships, inventory cycles, regional product preferences, and retail visibility across India requires a very different operational model compared with digital-first scaling.

Investors are likely to monitor whether Honasa can maintain both growth momentum and margin expansion over the coming quarters.

What Lies Ahead for Honasa Consumer

The company appears focused on three major priorities going forward:

1. Deepening Offline Penetration

Offline retail expansion remains central to long-term growth, especially in Tier II and Tier III markets.

2. Building a Multi-Brand Portfolio

Reducing dependence on a single flagship brand could improve resilience and category diversification.

3. Sustaining Profitability

The latest results indicate stronger operational discipline, but consistency will be key to sustaining investor confidence.

If Honasa continues balancing growth with profitability, it could emerge as one of the few scaled Indian D2C beauty companies successfully transitioning into a broader FMCG-style operating model.

Conclusion

Honasa Consumer’s FY26 fourth-quarter performance marks an important milestone in the company’s post-listing evolution.

The sharp rise in profit, record quarterly revenue, expanding EBITDA margins, and first-ever dividend collectively suggest a business moving beyond pure growth-at-all-costs toward more sustainable execution.

The company still faces competitive and operational challenges, but its latest numbers indicate improving fundamentals at a time when investors are increasingly rewarding disciplined growth.

For India’s broader startup ecosystem, Honasa’s performance may also represent a larger trend: digital-first consumer brands are now being evaluated not just on visibility and growth, but on their ability to build durable, profitable businesses.

Also Read : Damroo Raises Rs 5 Crore Investment to Scale Artist Growth Across India

Last Updated on Friday, May 22, 2026 1:10 pm by Startup Newswire Team