Introduction

For nearly two decades, India’s startup narrative revolved around a familiar map: Bengaluru for SaaS, Gurgaon for consumer internet, Mumbai for fintech, and Hyderabad for enterprise technology. Venture capital, engineering talent, startup accelerators, and media attention remained concentrated in a handful of urban clusters.

That concentration is beginning to change.

A new generation of Indian B2B startups is emerging from cities traditionally viewed as peripheral to the country’s technology economy — Indore, Jaipur, Kochi, Coimbatore, Surat, Lucknow, Ahmedabad, Bhubaneswar, Nagpur, and Chandigarh among them.

The shift is not accidental. It is being driven by structural changes in India’s economy: manufacturing decentralisation, logistics expansion, digitisation of SMEs, lower operating costs, improved internet infrastructure, post-pandemic remote work culture, and rising entrepreneurial ambition outside metro ecosystems.

Unlike the consumer-tech wave of the 2010s, many of these newer companies are solving operational problems rooted in India’s real economy — warehousing, industrial procurement, supply-chain software, manufacturing workflows, rural distribution, B2B commerce, and enterprise automation.

In many ways, this is less glamorous than the unicorn era dominated by food delivery and quick commerce. But it may ultimately prove more durable.

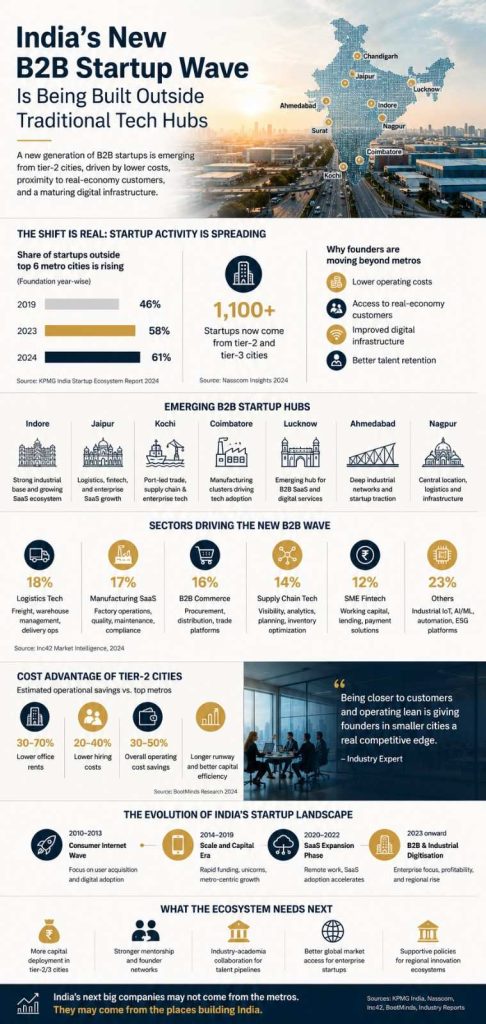

India’s Startup Geography Is Expanding

India’s startup ecosystem is no longer overwhelmingly metro-centric.

Recent industry analyses indicate that a growing share of new startups are now originating outside the country’s top six metro cities. According to ecosystem reports and industry trackers, tier-2 and tier-3 cities are becoming increasingly active across SaaS, logistics, industrial technology, agritech, and enterprise software segments.

The reasons are deeply economic.

Cities like Jaipur, Indore, Kochi, Coimbatore, and Visakhapatnam now offer:

- lower commercial real-estate costs

- access to engineering colleges and technical talent

- improving digital infrastructure

- expanding industrial ecosystems

- growing SME clusters

- lower employee attrition than metro hubs

- proximity to operational customers

This matters particularly for B2B businesses.

Consumer internet startups often needed dense urban markets, rapid user acquisition, and venture-funded scale. B2B startups, by contrast, frequently need close integration with factories, distributors, warehouses, logistics operators, and industrial customers.

That changes where companies are best built.

Why B2B Startups Are Moving Beyond Bengaluru

1. The Customer Base Is Outside Metros

India’s industrial economy is geographically dispersed.

Manufacturing clusters are spread across Gujarat, Rajasthan, Tamil Nadu, Punjab, Maharashtra, Uttar Pradesh, and Andhra Pradesh. Logistics corridors increasingly extend through emerging warehousing hubs rather than only traditional metros.

Industry reports from JLL and logistics researchers show strong warehousing expansion in cities including Jaipur, Lucknow, Kochi, Nagpur, Coimbatore, and Chandigarh-Rajpura.

For founders building:

- logistics SaaS

- industrial procurement platforms

- B2B commerce networks

- manufacturing automation tools

- SME digitisation software

- supply-chain intelligence platforms

…being physically closer to customers can be strategically valuable.

Many enterprise founders now argue that spending time near factories and distributors offers more insight than remaining embedded within metro startup ecosystems.

2. Cost Structures Are Far More Sustainable

One of the biggest pressures facing Indian startups over the past three years has been the rising cost of talent and operations in major cities.

Bengaluru and Gurgaon remain important startup hubs, but salary inflation, office rentals, and hiring competition have significantly increased operational burn for early-stage companies.

Tier-2 cities offer a different equation.

Some ecosystem studies estimate operational advantages of 30–70% compared with metro startup hubs, depending on role type and business model.

For B2B startups that prioritise profitability, longer cash runways, and sustainable growth, that difference can be transformative.

This is particularly relevant in the post-2022 funding environment, where investors increasingly emphasise revenue quality and capital efficiency over aggressive expansion.

3. Remote Work Changed Founder Behaviour

The pandemic accelerated a broader behavioural shift among Indian founders and employees.

Thousands of professionals left Bengaluru, Mumbai, and Gurgaon during the remote-work years. Many never returned permanently.

This created a new generation of startup operators comfortable building companies from smaller cities while maintaining distributed teams and national client bases.

For enterprise startups, this decentralisation became operationally viable because:

- SaaS infrastructure became cheaper

- cloud collaboration tools matured

- enterprise sales moved online

- digital payments became ubiquitous

- video-first workflows became normal

As a result, founders no longer needed to remain inside traditional tech corridors to access customers or talent.

The Rise of “Practical B2B”

One of the defining features of India’s new non-metro startup wave is its operational pragmatism.

These startups are often solving highly specific industry problems rather than chasing broad consumer scale narratives.

Examples include:

- warehouse workflow automation

- procurement digitisation

- freight management

- industrial quality software

- SME financing infrastructure

- inventory management systems

- B2B supply-chain platforms

- manufacturing SaaS

- regional distribution networks

The businesses may not always generate headline-grabbing valuations early on, but many are targeting sectors with deep inefficiencies and long-term revenue potential.

This reflects a broader maturation of India’s startup ecosystem.

The first generation of Indian internet startups largely focused on digital consumer adoption. The next generation increasingly appears focused on digitising India’s economic infrastructure itself.

Logistics and Manufacturing Are Driving the Shift

The expansion of India’s logistics and manufacturing sectors is playing a central role in this transition.

Government infrastructure investments, industrial corridors, warehousing expansion, and supply-chain diversification are creating new commercial ecosystems outside major metros.

Recent warehousing industry data indicates rapid growth across several tier-2 logistics centres, including Jaipur, Lucknow, Kochi, and Nagpur.

Simultaneously, manufacturing digitisation is creating demand for:

- factory management software

- predictive maintenance tools

- industrial IoT systems

- procurement automation

- compliance and quality platforms

This is creating fertile ground for enterprise startups rooted in operational industries rather than purely digital markets.

Companies such as ElasticRun have demonstrated how logistics and rural distribution networks can be built around underserved markets rather than only metro consumption centres.

Similarly, industrial software firms from emerging cities are increasingly gaining traction among enterprise customers seeking India-specific operational solutions.

Investors Are Slowly Following the Trend

Venture capital still remains heavily concentrated in Bengaluru, Mumbai, and Delhi NCR. However, investor interest in non-metro startups is clearly increasing.

Several early-stage funds now explicitly focus on tier-2 and tier-3 founders.

The investment thesis is straightforward:

- lower burn rates

- stronger founder retention

- underserved SME markets

- proximity to industrial customers

- rising regional digitisation

- improving infrastructure

Importantly, many investors now recognise that India’s next major enterprise opportunity may not emerge from another consumer app.

It may emerge from software that helps Indian businesses operate more efficiently.

That is a significantly larger long-term economic opportunity.

The Challenges Remain Real

The decentralisation of India’s startup ecosystem is still incomplete.

Founders outside traditional hubs continue to face structural disadvantages, including:

- weaker access to institutional capital

- smaller angel investor networks

- fewer experienced startup operators

- lower media visibility

- limited access to global enterprise networks

- reduced mentorship density

Recruiting senior leadership talent can also remain difficult outside metro ecosystems.

Many founders still eventually establish commercial offices in Bengaluru or Gurgaon for enterprise sales and fundraising, even if product or operations remain elsewhere.

The ecosystem shift is therefore evolutionary rather than revolutionary.

Traditional hubs still matter enormously.

But they are no longer the only credible centres for startup creation.

Why This Trend Matters for India’s Economy

The rise of non-metro B2B startups has implications beyond venture capital.

It signals a broader decentralisation of India’s innovation economy.

Historically, startup growth remained concentrated within a few urban enclaves. If enterprise innovation increasingly spreads across smaller cities, it could:

- create higher-skilled regional employment

- strengthen local manufacturing ecosystems

- deepen SME digitisation

- reduce migration pressure on metros

- improve regional economic participation

- accelerate formalisation of smaller businesses

This aligns with broader economic trends already underway across warehousing, infrastructure, manufacturing, and digital commerce.

In effect, India’s startup ecosystem may finally be starting to resemble India’s actual economic geography.

The Future Outlook

The next five years could reshape how India defines a “startup hub.”

Bengaluru will likely remain India’s dominant technology centre. But the monopoly of a few metros over startup creation appears to be weakening.

The strongest opportunities may increasingly emerge from founders building closer to real operational problems:

- factories in Coimbatore

- logistics corridors in Jaipur

- industrial clusters in Gujarat

- SME ecosystems in Indore

- port-linked trade networks in Kochi

- manufacturing supply chains across Tier-2 India

India’s next major B2B companies may therefore look very different from the startup icons of the previous decade.

They may grow slower.

They may raise less capital initially.

They may avoid consumer hype cycles.

But they may also build more resilient businesses.

Conclusion

India’s startup ecosystem is entering a quieter but potentially more consequential phase.

The new wave of B2B startups emerging from tier-2 and tier-3 cities reflects deeper shifts within the Indian economy itself — decentralised manufacturing, regional consumption growth, logistics expansion, SME digitisation, and operational technology adoption.

This is not merely a geographic shift.

It is a philosophical one.

The centre of gravity in Indian startups is gradually moving from attention-driven growth toward infrastructure-driven value creation.

And increasingly, that future is being built outside traditional tech hubs.

Also Read : How AI Agents Could Reshape India’s Startup Workforce Over the Next Five Years

Last Updated on Wednesday, May 20, 2026 11:14 am by Startup Newswire Team

{kind=link}